The AI sector is increasingly characterised by interwoven financial and operational relationships, where companies act simultaneously as suppliers, customers, and investors. This has led to what analysts call a “circular economy” in AI infrastructure:

At the centre of this digital ouroboros is OpenAI, the once non-profit darling turned corporate juggernaut, now entangled in a web of billion-dollar deals that would make even Wall Street blush.

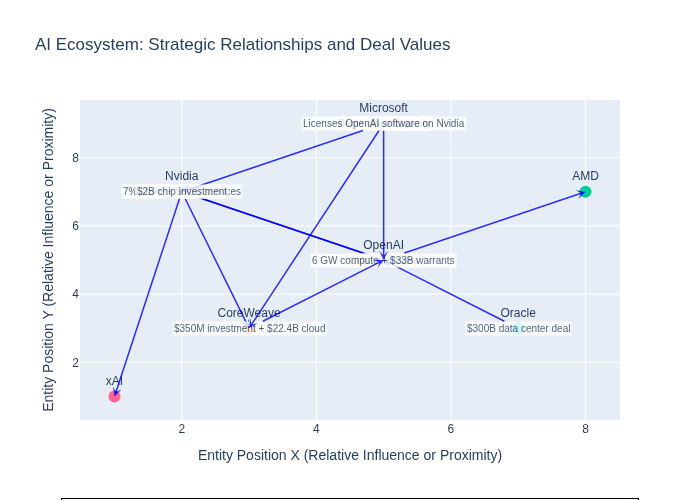

Let’s start with the obvious: OpenAI has secured a staggering $100 billion infrastructure commitment from Nvidia. That’s not a typo. One hundred billion dollars. In return, OpenAI is buying millions of Nvidia’s chips to power its AI models. It’s a neat little loop—Nvidia funds the infrastructure, OpenAI buys Nvidia’s chips, and everyone’s stock price gets a nice little bump. Circular economy? More like circular logic.

But wait, it gets better. Oracle, not wanting to be left out of the AI arms race, inked a $300 billion deal with OpenAI to build data centres using—you guessed it—Nvidia and AMD chips. So now we have Oracle building the house, Nvidia supplying the bricks, and OpenAI renting the rooms. It’s like a tech version of Monopoly, except the players are all lending each other money to buy properties they already own.

Then there’s AMD, the underdog trying to claw its way into the AI chip market. OpenAI, ever the savvy operator, struck a deal for 6 gigawatts of compute power using AMD’s MI450 chips. In exchange, OpenAI gets warrants to buy up to 10% of AMD’s stock—worth a cool $33 billion if AMD’s share price hits $600. That’s right: OpenAI is now financially incentivised to pump AMD’s value, while simultaneously being Nvidia’s biggest customer. Conflict of interest? Only if you’re still clinging to the quaint notion of corporate independence.

And let’s not forget CoreWeave, the cloud infrastructure company that’s become the connective tissue in this techno-cabal. Nvidia owns 7% of CoreWeave and has committed $6.3 billion in service purchases. CoreWeave, in turn, has invested $350 million in OpenAI and signed cloud agreements worth $22.4 billion. It’s a beautiful triangle of mutual back-scratching, where money flows in a circle and accountability disappears into the ether.

Hovering above it all is Microsoft, OpenAI’s largest shareholder and its most enthusiastic cheerleader. Microsoft licenses OpenAI’s software, which runs on Nvidia hardware, and rents cloud capacity from CoreWeave. So Microsoft is paying OpenAI, which pays Nvidia, which funds CoreWeave, which serves Microsoft. It’s like a tech version of a Rube Goldberg machine—only instead of marbles and levers, it’s powered by shareholder equity and GPU clusters.

And just when you thought the cast of characters couldn’t get any more colourful, enter Elon Musk’s xAI. Nvidia is reportedly investing $2 billion in Musk’s latest venture via a special purpose vehicle (SPV) to buy chips that will be rented out over five years. Because nothing says “sound investment strategy” like giving Elon Musk a blank cheque and hoping for the best.

Complicated I hear you say? You bet! And worrying if you ask me! The amounts of money involved are enormous – while AI is potentially still eons away from being widely adopted in particular in the corporate world and from making any meaningful financial returns on these colossal investments.

Now, let’s pause and ask the obvious question: what could possibly go wrong?

Well, history offers a few cautionary tales. Remember WeWork? A company that raised billions on the promise of “revolutionising workspaces,” only to implode under the weight of its own hype and incestuous funding. Or Theranos, where investors, dazzled by charisma and buzzwords, poured money into a black box that never worked. These weren’t just failures—they were systemic breakdowns enabled by a lack of scrutiny and a surplus of mutual admiration.

The AI ecosystem is starting to look eerily similar. When companies are simultaneously investors, customers, suppliers, and competitors, the lines between due diligence and blind faith blur. Valuations become self-reinforcing illusions. Risk is no longer distributed—it’s concentrated in a handful of players who are all betting on each other’s success.

This isn’t just a financial house of cards; it’s a technological monoculture. If one node in this network falters—say, Nvidia’s chip supply chain collapses, or OpenAI’s models hit a wall—the ripple effects could be catastrophic. Innovation stalls. Capital evaporates. And the same companies that once propped each other up will start dragging each other down.

In theory, competition is supposed to drive progress. But in this brave new world of AI, we’re seeing the opposite: a consolidation of power, a homogenisation of infrastructure, and a dangerous dependency on a few key players. It’s not a free market—it’s a feedback loop.

So the next time you hear about a multi-billion-dollar AI deal, don’t be dazzled by the zeroes. Ask yourself: who’s really paying? Who’s really benefiting? And who’s holding the bag when the music stops? Because if history has taught us anything, it’s that when everyone’s betting on each other, the only sure thing is that someone’s going to lose.

It’s difficult to imagine anything here that doesn’t end in a loud “pop”. But then you realise that the end game here isn’t to deliver something, but to get rich by adding hype to the mix.

LikeLiked by 1 person

I suppose the jury is still out on how much AI really will benefit society, but in the meantime, as you say, some people and organisations are minting it…

LikeLike